STEVE G wrote:kalbow wrote:Whaler wrote:

Keeping it simple and as crude budget you need account for doubling your monthly/annual budget every 10 years assuming this is savings that also earn interest.

Whaler, presumably the doubling of a budget amount you quoted is as a result of currency fluctuations right? Otherwise, are we saying that inflation is running around 8.5% per annum in LOS?

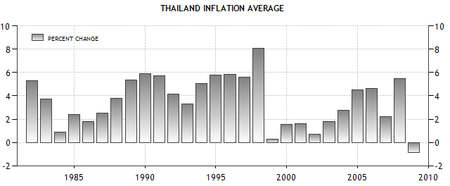

It's at about 4% at the moment but it did go over 8% in 2008.

Yes, and I worked out the average going back to the 80's is about 3.9%, but as you can see from the graph it's a bit rollercoaster. IMO, inflation is the unexpected killer that can screw people up, there's an excellent post/thread here by m_right:

HHAD Inflation Thread

- trytrtryty.jpg (15.36 KiB) Viewed 2186 times

Inflation:

The OP asked for costs of living 'today' basically so that's fair enough, but for anyone who is looking at budgeting for the rest of their lives, and any of the following is part of their budget plans, then they need to seriously consider factoring in inflation... a) a lump sum in a saving account, b) an income from pension or other that's growth is dependant upon index-linking, and c) anyone renting.

Examples of why I think it's a massive gamble to rely on stuff like

'90,000 Baht/month is more than enough to live comfortably'...

1)

Overseas Based Income: Based on historical averages over the past 30-50 years of Thai & UK inflation rates, if you're income is from a UK index-linked pension, in 30 years time your income will have 'devalued' by 31%, so 90k/month is only 62k/month. That's without sudden recessions/exchange rate disaster that HHF has been talking to a brick wall about. That's without Hua Hin taking back off again, over-and-above national inflation, after this recession is over, a nailed-on dead cert in a popular, developing resort. Either of these occurs and the 62k will be maybe 55k!?

Future Growth of UK 'Index-Linked' Pensions to Reduce Due To Switch from RPI to CPI

2)

Renting: Based on same Thai & UK historical inflation and average UK property prices (rents generally track this) since 1971, then rental growth would have out-stripped your income growth by 7.6x, as property prices out-stripped inflation by 7%, ie: 7% extra-over inflation. So if you want the same 12k/month property you are renting today, you need to allow 91k/month in your budget for it,

today. And these figures do include the recent property 'correction' due to recession, but as it's based on a 40 year old starting point I'd agree it's unlikely prices will increase same as UK did. But even half of this would be pretty drastic I would have thought.

SJ